Finding the right rate of return for your community bonds will be critical to both your campaign success, and ultimately, your project success. Of course, it will be to your benefit to keep your cost of capital as low as possible. But at the same time, you will need to position an attractive investment to engage your community and ensure that you raise the capital you need.

Finding this balance is our specialty. Through a combination of financial modelling and community consultations, we help the organizations that we support to design bond terms that work for their balance sheet and their community.

Today we sat down with Mary Warner, the Co-Executive Director of Tapestry, to give you more insight into the process of crafting community bond terms. Below, she answers a few questions that recently came up during one of our Community Bond Workshops that we offer to non-profits, charities and co-operatives.

What is the typical rate of return offered on a community bond?

“Bond rates that we’ve seen typically range at the low end from 3%, to about 7% at the high end.

We’ve seen bond interest decrease slightly with the pandemic and current economic situation, but issuers do want to provide their investors with a decent rate of return for the risk they are taking on. So, we haven’t seen rates drop as significantly as commercial interest rates. Current rates for community bonds are averaging at about 3.5-5%.

Typically, the longer the bond term, the higher the interest rate. Another important note, is that when we are referring to interest here, we are speaking of simple interest – where the interest is paid out and does not become part of the principal. Compounding interest (where interest does become part of the principal) is possible in community bonds, but more complex and expensive to issuers. So, for the most part, we see simple interest with community bonds.”

How can we figure out how much we can afford to pay out?

“This is when our financial modelling comes in. The first step is putting together a business model with projections of the next 5-10 years, incorporating your new project.

Then we piece in different options for community bond rates and terms, based on your needs and early assessments of your community. It’s sort of a trial and error process of testing the community bond interest expense and principal repayment. Ultimately, we want to land on a few options that income and cash flow statements can bear.”

Can greater impact mean lower returns?

“That’s a really good question. We have seen in the past that investors may be willing to take a lower return if they feel a strong connection to the project and are passionate about the impact.

It’s really about finding a balance between the social and environmental return, and the financial return. If the impact is significant and important to the issuer’s community of supporters, you may find that investors are willing to take a slightly lower rate of return.

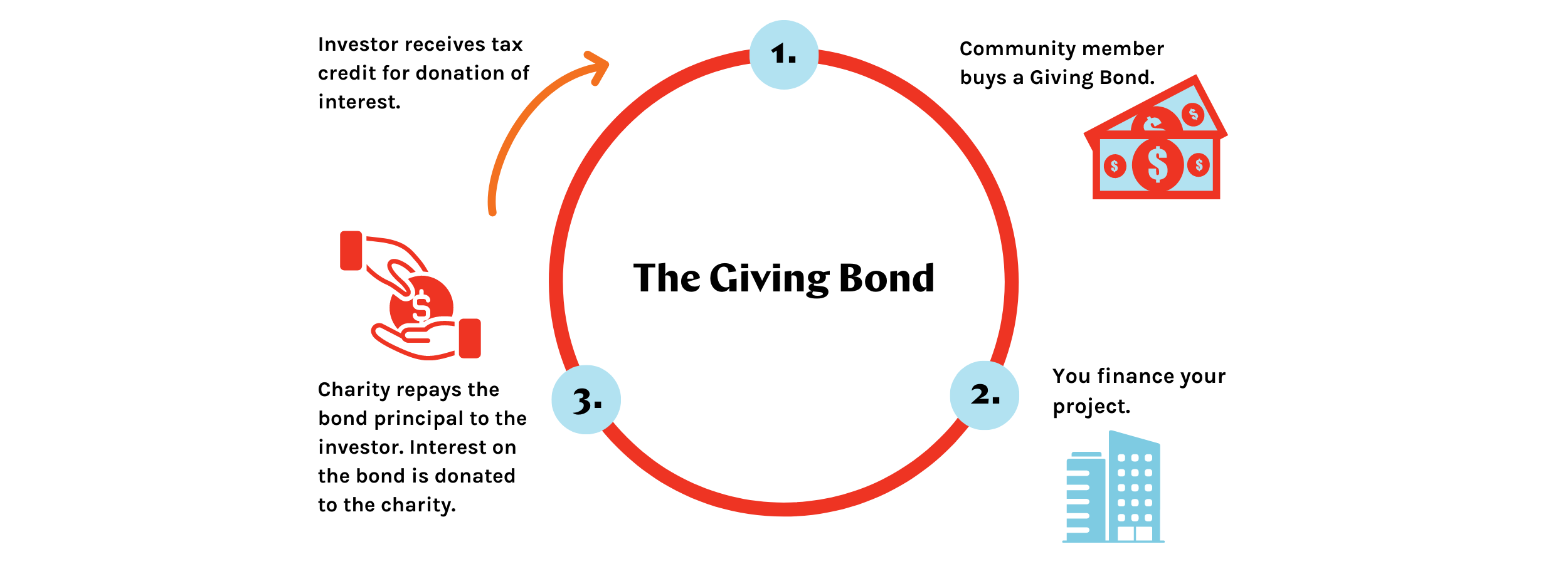

If you are a charity, you might also be interested in looking at the ‘giving bond’ model. This is where investors invest an amount of principal, but instead of receiving interest back as a payment to them every year, the interest is donated back to the charity. The investor does take on the income tax implications of having investment income but they get the benefit of a charitable receipt for the amount of money they donate.

So essentially, it’s equivalent to baking in an annual donation to the charity, and on the flip side, offering the charity an interest free loan. At the end, investors get their full principal investment back.”

We are afraid that we might need a few years to get up and running and generate a profit. Will that be a problem for us in issuing bonds?

“Not necessarily. When we are doing financial models, we want to see that there is the potential to pay back bonds at the end of their term. If your project will take a few years to generate the income necessary, we might want to look at a longer period bond. On the short end, there are 3 year bonds, on the longer side you could be looking at 7-15 years.

There are also different ways of paying out interest. You might choose to withhold interest payout until year four for example, or to simply pay out all the interest upon maturity. Those are just some of the options we have to manage your cash flow.

It’s completely normal that in the first year or two you might not generate consistent income until you are steadily up and running. What we want to see in the financial model is that in the longer term, these bonds can be repaid.”

We would like to have a 10 year bond, but we are worried that investors won’t want to keep their money tied up that long. Any suggestions?

What we’ve seen in the past with other issuers, is that it’s good to offer investors a mix of bond options. So, if we are offering a longer term bond, we might also want to offer a shorter term option. Some investors are able and willing to invest in a 10 year + bond and others will look for a shorter investment.

Having at least two series of bonds with different terms and rates can help with marketing efforts and give options to investors with different motivations. The added benefit of having multiple options is that it can allow you to stagger your principal repayments.

When it comes to a shorter term bond, there is also the option to refinance bonds at maturity. Often, our issuers who issue shorter bonds will choose to issue a new offering statement once their bonds have matured and ask investors to reinvest their funds. We see issuers having very high reinvestment rates. For example, our client SolarShare has found that when bonds reach maturity, about 60-70% of investors choose to reinvest their funds.”

Is there a possibility to repay the principal before the end of the bond term?

“Yes, typically in the offering statement there is a clause that will allow organizations to pay out the principal early. But there is a lot to consider in making this decision. It can sometimes be to the benefit of organization, allowing them to save on interest costs. But it’s also important to consider the relationship you have with your investors.

It may sour the relationship if investors expected this investment for a period of time and they no longer receive interest payments because you decided to repay the principal early. So yes, there is the possibility but the consideration should not so much be ‘can we?’ but ‘should we?’.

In the case of investor need, the offering statement or the Board can set out the terms of how an “early redemption” takes place. In some cases it may not be possible, in others you might consider allowing an early redemption if the investor provides a letter stating financial hardship and requesting a redemption prior to maturity.”

We work in a low income neighbourhood and it is important to us that we include our community in this campaign. How can we do that?

“Economic inclusion is a really important topic, and for most of our issuers it’s very important that bonds are accessible to a wide range of their community. We have seen bond minimums set as low as $500 to make this possible.

We have also had discussions with issuers where they want to maximize community participation by limiting larger size investments. While the logistics of managing 5 $100,000 bonds may be simpler than managing 500 $1,000 bonds, many issuers we work with have consistently chosen to make community bonds as accessible as they can, setting low minimums for investment and carefully considering larger investments. Community bonds are always about more than financial returns, both for the issuer and the investor.“

How do community consultations help in finding the right rate of return?

“Community consultations give you the opportunity to go to your stakeholders and see what they think of your bond terms and find out what is most attractive. This can help us decide on the options to include in your offering statement. Sometimes you will find that one bond series might resonate better than others.

You are never going to be able to speak to everyone, but we can help you select a representative group of your community and gain crucial feedback early on to see what is going to be attractive once you start selling. This also allows you to bring stakeholders together early and start to build enthusiasm and excitement about the project you are working towards.”