Across Canada, communities are facing the dual crisis of rising housing costs and the disappearance of accessible, inclusive spaces. And while headlines may differ from province to province, the underlying challenges – displacement, disinvestment, and inaction – are all too familiar.

Take Québec for example, a province where the housing crisis is made especially visible each year through a long-standing tradition.

Every year on July 1st, a uniquely Québécois ritual unfolds: Le Jour des déménagements, or Moving Day. Originally designed to avoid uprooting school-aged children mid-year, it has become a striking symbol of housing precarity. On this day, tens of thousands of leases expire across the province – sending renters scrambling to move, often with few affordable options.

In 2024, that precarity reached new heights.

The provincial rental board recommended a rent increase of 5.9%, the highest in decades. Actual rent hikes, especially in units with turnover, are even higher. Evictions across Québec have increased six-fold since 2020 – and that’s only counting reported evictions. In response, housing advocates recently launched a province-wide “week of action”, including the occupation of a vacant, city-owned building that had been promised for social housing – but still sits empty.

Public programs for social housing have been defunded, and few new options have replaced them. Communities are left wondering: What tools do we actually have? That’s where Brique par Brique comes in.

A community that isn’t waiting

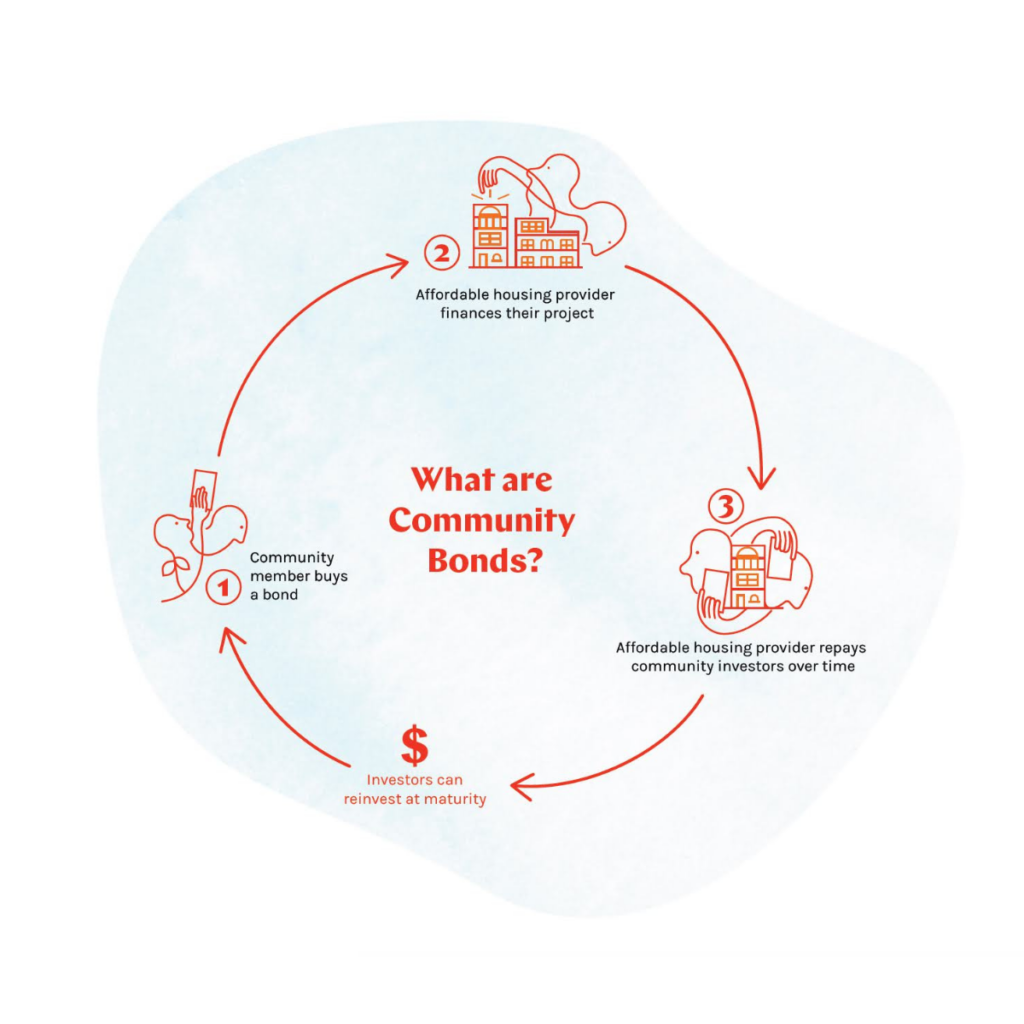

Rather than waiting on delayed public programs, Brique par Brique, a community organization in Parc-Extension, is mobilizing the power of collective investment. Their $5 million community bond campaign is raising capital to support two critical projects:

- A permanently affordable, non-speculative housing development

- A Centre for Creative & Collective Action that offers space for programming, culture, and community organizing to support organizations working to combat social inequities

This campaign isn’t just about raising capital. It’s about building power. By inviting residents to co-invest in their own community, Brique par Brique is creating a model of co-ownership, connection, and shared responsibility.

This isn’t new in Québec

What makes this campaign especially powerful is that it’s grounded in Québec’s long-standing tradition of collective organizing in response to austerity and government retreat. From the rise of co-operatives and caisses populaires (credit unions) to the growth of solidarity unions, Québec communities have long created tools to fill the gaps left by underfunded public systems and market failures. These were tools that gave people control when institutions didn’t.

In fact, while the term “community bond” gained prominence later in Ontario, Québec was home to one of the earliest examples of this kind of financing. In the early 2000s, residents of Sorel-Tracy mobilized local capital to fund a new recreation centre. That campaign helped lay the groundwork for community-led finance models.

Brique par Brique is continuing that legacy. Their campaign doesn’t just use a financial tool; it reclaims one as a vehicle for community power, mutual aid, and long-term stewardship.

Why it matters – even beyond Québec

You don’t have to live in Québec or work in housing to learn from this.

Brique par Brique’s campaign illustrates a powerful truth: when systems fall short, communities can still lead.

Community bonds aren’t the only answer. But they are a promising one, especially when used by organizations with deep relationships, aligned values, and a clear long-term vision. When done right, community bonds can spark agency, organize communities, and help build infrastructure that truly reflects the people it’s meant to serve.

At a time when non-profits across Canada are struggling with stalled funding, rising costs, and increased demand, Brique par Brique shows what’s possible when we stop waiting and start building – from the ground up.

Learn more about Brique par Brique’s community bond campaign here.

Commentaires récents